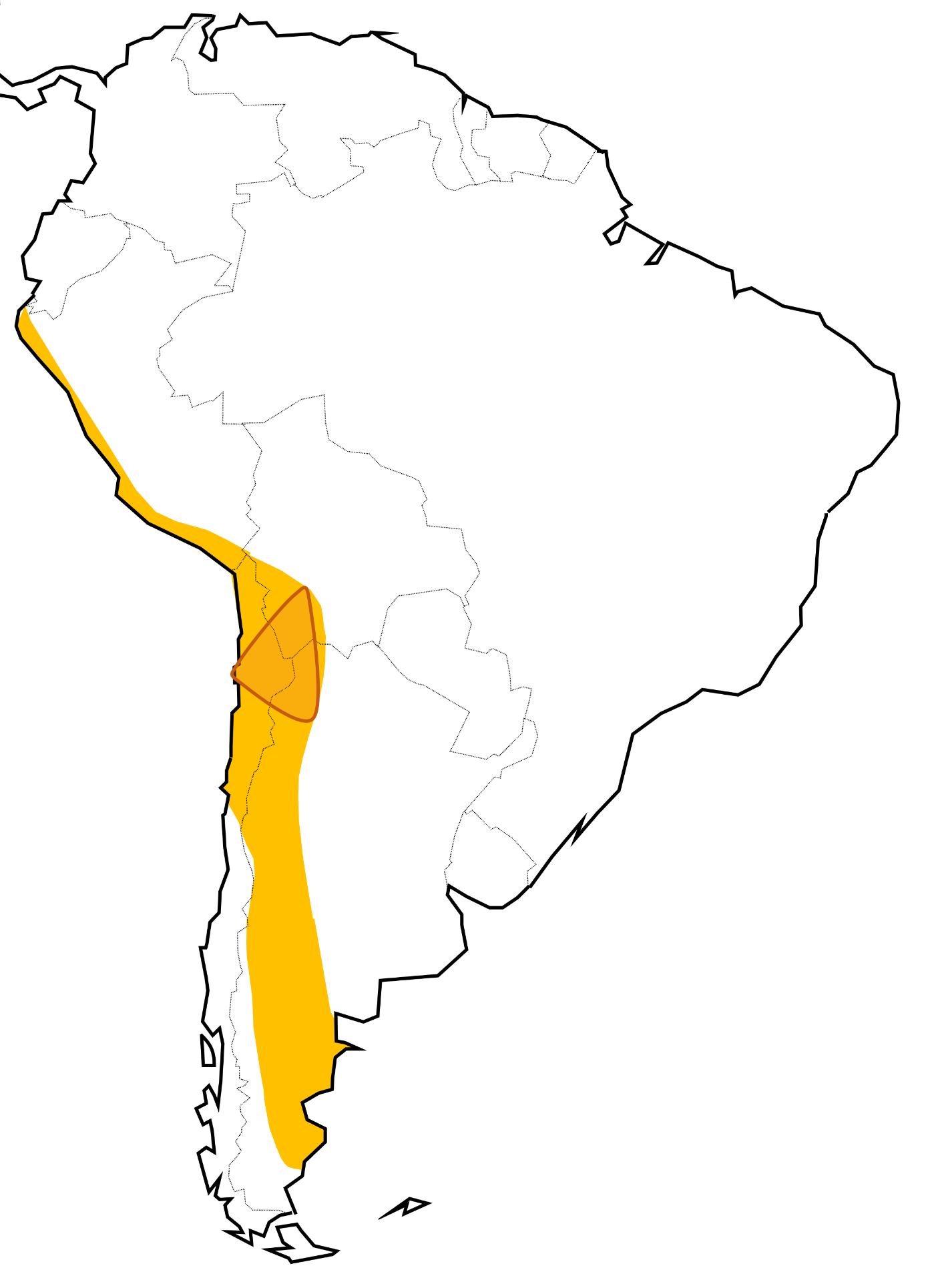

The Lithium Triangle — the high-altitude salt flats spanning Bolivia, Argentina, and Chile — holds an estimated 56 % of the world's identified lithium resources. It currently produces roughly 30 % of global lithium output. The gap between resource and production is the most consequential supply-chain story in the EV transition.

Geology dictates timeline

Triangle lithium sits in subterranean brines under salt flats (salars), not in the spodumene hard-rock ores found in Australia. Brine extraction historically used solar evaporation ponds — cheap operating cost but slow (12-24 months from pumping to battery-grade lithium carbonate) and water-intensive in fragile high-desert ecosystems.

Direct Lithium Extraction (DLE) technologies emerging since 2020 promise faster cycle times and lower water use, but at higher capex and unproven recovery rates at production scale. The choice of extraction method per project is now a major strategic variable.

Three different policy regimes

- Chile nationalized lithium under Boric in 2023 — not Soviet-style but state-controlled with private operating partners. SQM and Albemarle dominate production; future projects route through state company Codelco. Investment has slowed.

- Argentina took the opposite path — Milei's regulatory liberalization in 2024 reduced provincial royalties and approved fast-track projects. Output is growing faster than Chile but governance is unstable across electoral cycles.

- Bolivia has the largest reserves (Salar de Uyuni) and the smallest production. State control under YLB has produced repeated false starts; first-of-kind DLE pilots with Chinese partners (CATL, Citic Guoan) and Russian (Uranium One) are commissioning in 2025-2026.

Water as the binding constraint

Salar lithium extraction consumes ~500,000 liters of water per tonne of lithium carbonate equivalent in conventional evaporation pond projects. The salars sit in arid high-altitude regions where indigenous communities depend on the same aquifers. Water-rights disputes in Atacama (Chile) have repeatedly delayed projects and contributed to the political case for nationalization.

DLE could reduce water use 60-90 %, which is why the technology has policy relevance disproportionate to its current production share.

Demand-side dynamics

EV battery chemistry is bifurcating. Lithium iron phosphate (LFP) — Chinese-dominated, no nickel/cobalt — is taking share in mass-market vehicles. Nickel-rich NMC (nickel-manganese-cobalt) chemistries hold the long-range premium segment. Both use lithium; the difference is whether the marginal demand is stable or volatile, and how much lithium per kWh each uses.

Chinese refining still handles the majority of triangle output, even when extraction is by Western operators. This creates the same processing-vs-mining asymmetry seen in rare earths: physical material in one geography, technical leverage in another.